On 1st Jul 2017, India introduced Goods and Services Tax (GST) after almost a decade of deliberation and is the biggest indirect tax reform undertaken since independence and is also the biggest digitization of tax infrastructure in the world. To keep things into perspective let’s see numbers

16 different taxes were subsumed under GST, 6 covered by Central Government & 10 covered by 28 different State government and was touted as One Nation One Tax. One of the most trusted Indian company was entrusted with the task to develop the digital infrastructure.

GST is in place for 2 ½ years now and has its fair share of critics. The Indian economy has slowed down to its lowest level in a decade and most economist and businesses believe GST and its botched implementation to be one of several reasons. The compliance level is low, revenue targets are not met and businesses are still figuring out the most efficient way to manage this disruption. We all knew it would not be easy and there will be a lot of teething trouble and the same is happening

I will be discussing pain areas and ways to make this transition less taxing on businesses and the economy. I will keep my discussion restricted to non-technical aspects for general discussion purposes.

Tax certainty / Predictability of law:

Over the last 2 years, GST law was amended over two hundred times. A new law will require changes and a proactive approach to problem-solving is the cornerstone for success. However, this volume of changes has led to confusion and uncertainty in the minds of business community. Businesses need certainty in tax policies to plan and then implement. A recent case in point is the availment of input credit which was 1st restricted to 20% and then 10%.

One of the ways we can mitigate unintended consequences is by floating a draft amendment before final notifications. The same happened in past when budgets were presented and became laws post deliberation. Secondly, procedural changes could be implemented in stages and voluntarily to start with

Digitization & micromanagement

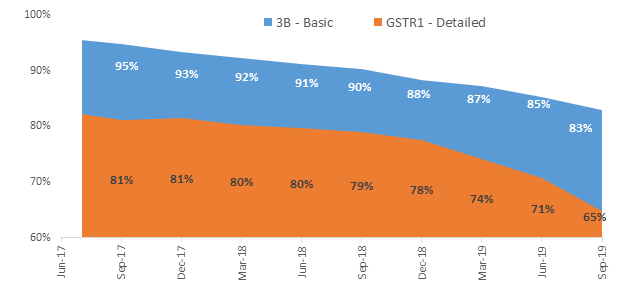

GST is supposed to be 100% digitized law and had a novel idea of tracking compliance digitally. This led to high compliance cost for small business. An annual $ 120 increase in compliance cost from the perspective of India’s $2,500 per capita income seems high. In the zeal of controlling the entire business process and to eliminate tax evasion government introduced a lot of procedural details, starting with monthly returns to now e-way bills and digital invoicing. The intention of making it evasion proof has made the procedure cumbersome and expensive to comply. The intention of the government to track every transaction on an item level (it does make sense) doesn’t factor in the ground realities and business dynamics. The IT change management infra is not fast enough to update itself with changing business needs. The below chart proves my point wherein the level of compliance goes down as the compliance procedures increases.

Comparison chart of compliances done by business between 3B, GSTR

Only 70% of taxpayers file returns regularly. A major headache is, however, the mismatch between initial and final returns filed by taxpayers. There is an estimated mismatch of Rs 34,000 crore tax liabilities reported in GSTR-1 and GSTR-3B. The present GST structure has no mechanism for checking discrepancies found between GST Returns for July-Dec and Final Returns. About 84 % of the taxpayers were unable to correctly report revenue statements. The discrepancies and e-way bill failure demand that the GST Council now needs to take rigorous measures to tackle the menace of tax evasion through under-invoicing, non -invoicing etc.

The multiplicity of rates and lack of HSN code clarity

One of the biggest pain areas of earlier tax regime was the multiplicity of taxes and rates. Sadly this pain has crept into GST law and now instead of having 2 or 3 rates, we have a whole list of rates, cess, exemptions etc. Kerala has even added a cess for funding restructuring cost of a natural calamity. The revenue-neutral rate was 15% and now we have rates ranging from 1% to 42% (0, 0.1, 0.25, 1, 1.5, 3, 5, 7.5, 12, 18 and 28 percent + cess). Department has sent notices seeking products to be put in on higher tax brackets. Petroleum products, power, and real estate are still outside the GST ambit.

Then there is HSN code, it is the single biggest change and was meant to reduce product classification litigation. The HSN scheme introduced in GST was not able to fulfil this promise and a single product can be categorized on multiple HSN codes or a single HSN code can be grouped into multiple tax rates. Tax rates change based on packing or selling price eg clothes, hotels, dry fruits, a simple iron screw all can have different tax rates for the same service or product. This ambiguity needs to stop and simplified by tax administration even at revenue loss as it promotes compliances and will increase revenue in the long run.

Rules to tackle tax evasion

When it all started GST was structured to be a self-regulated compliance system. The IT infrastructure never lived up to expectation and a lot of procedures were toned down (Many of them were not needed in the first place and it seems were designed to kill evasion once and for all). Frequent changes, the backlash from the business community on unplanned implementation and general economic slow -down resulted in lower GST collections making matters worse. A revenue shortfall of Rs 60,000 crore is expected in the current fiscal year. Government has introduced more compliances to plug in gaps and had taken knee jerk action to stem downfall. A case in point is stopping of export refunds due to few fraud cases, sending cash flow issues for honest exporters. We have to remember 70 % of Indians don’t even have a smartphone in India and we pushing everyone to a digital environment will have a severe negative impact on smaller and marginal players. The policy flip flops and rollbacks have made GST a paradise for tax evaders, which has resulted in a lot of discourse between tax authorities and genuine businesses leading to stringent verification norms.

Excessive focus on the reconciliation of each entry in books and getting it certified has incentivized businesses to be small to avoid compliances and scrutiny.

Exemptions and Deemed taxability

The law as it stands lists multiple exemptions and additional liabilities based on nature of service provider increasing compliances. Then there is a deemed taxability of services provided by the corporate or regional office to branches, which although being revenue neutral has created extra compliances. This aspect lacks clarity on its applicability and methodology of calculations. One can even say that GST is being levied on employee salary because of this provision

Delay in refunds to Exporters and business under GST law has created working capital issues, which were not faced by the business due to various exemptions in the earlier regime. The promise was a seamless, no human intervention refund mechanism, which started on a good note but got derailed due to detection of frauds and a general shortfall in revenue collections.

Criminalization of procedural lapses

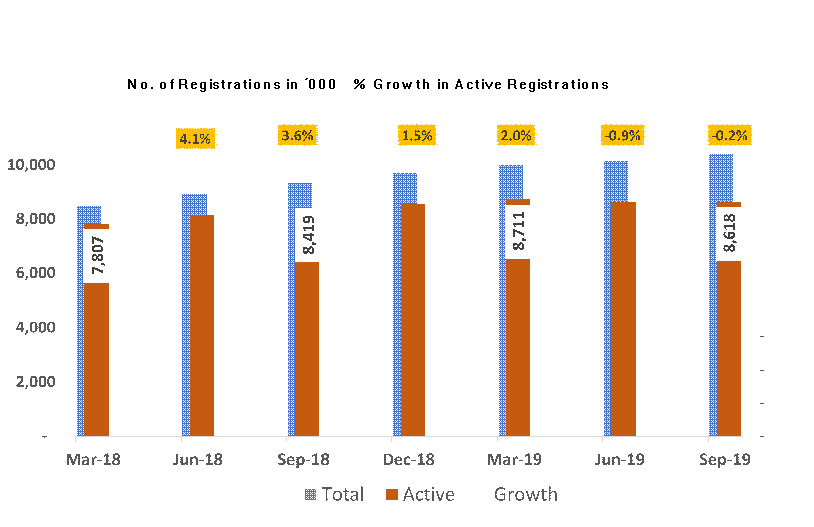

Over the last year amendments made in tax laws have given rights to officers to get the assessee arrested or get their bank accounts seized or get their GST registration suspended. These are all high handed methods of tax compliances which may lead to better compliances but can cripple small and medium enterprises. Below chart shows how the growth in new tax assesses have slowed and numbers degrowing for assesses who are filing basic monthly return